The Trade Deficit Blowout is as Predictable as My Dog Begging for Food at the Dinner Table

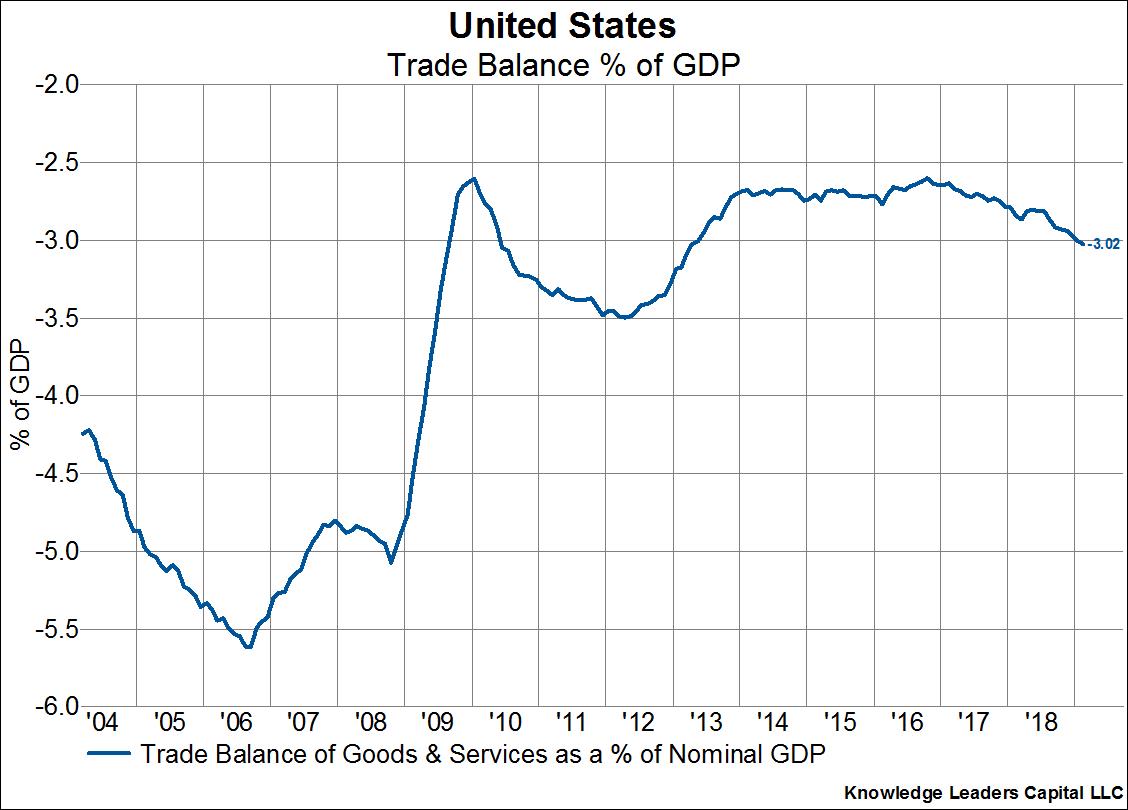

March 06, 2019The big news of the day relates to the continuation of a trend that has been going on since 2013: the widening of the trade deficit. The trade deficit in dollar terms at $-59.8bn in December and $-622bn for the year broke down to a new 10-year low. The trade balance as a percent of GDP at -3% broke down to a level not seen since 2013. Yes, these are big numbers, but they are entirely reflective of the economic policies pursued in this country and really shouldn’t come as much of a surprise. More important for our readers than that though, is the question of what this all means from an investment perspective. In this note we’ll cover both the why and what it means for financial markets.

Why is the trade deficit blowing out? It’s the result of simple math, really. Without going into the mathematical derivation, suffice it to say that:

T-G=(I-S) + (X-M), where T=taxes, G=government spending, I=investment, S=savings, X=exports and M=imports.

That is to say, the budget deficit equals investment minus savings plus net exports. In layman’s terms, if we run higher government budget deficits then either investment must fall and we must save more, we must import more than we export, or both. One way or another, someone has to foot the bill for higher budget deficits. That someone is either the domestic sector in the form of more savings and less investment or foreigners via importing capital (i.e. running larger trade deficits).

Therefore, if we put into place policies like tax cuts with investment incentives that end up resulting in higher budget deficits, then the corollary is a higher trade deficit. Simple enough.

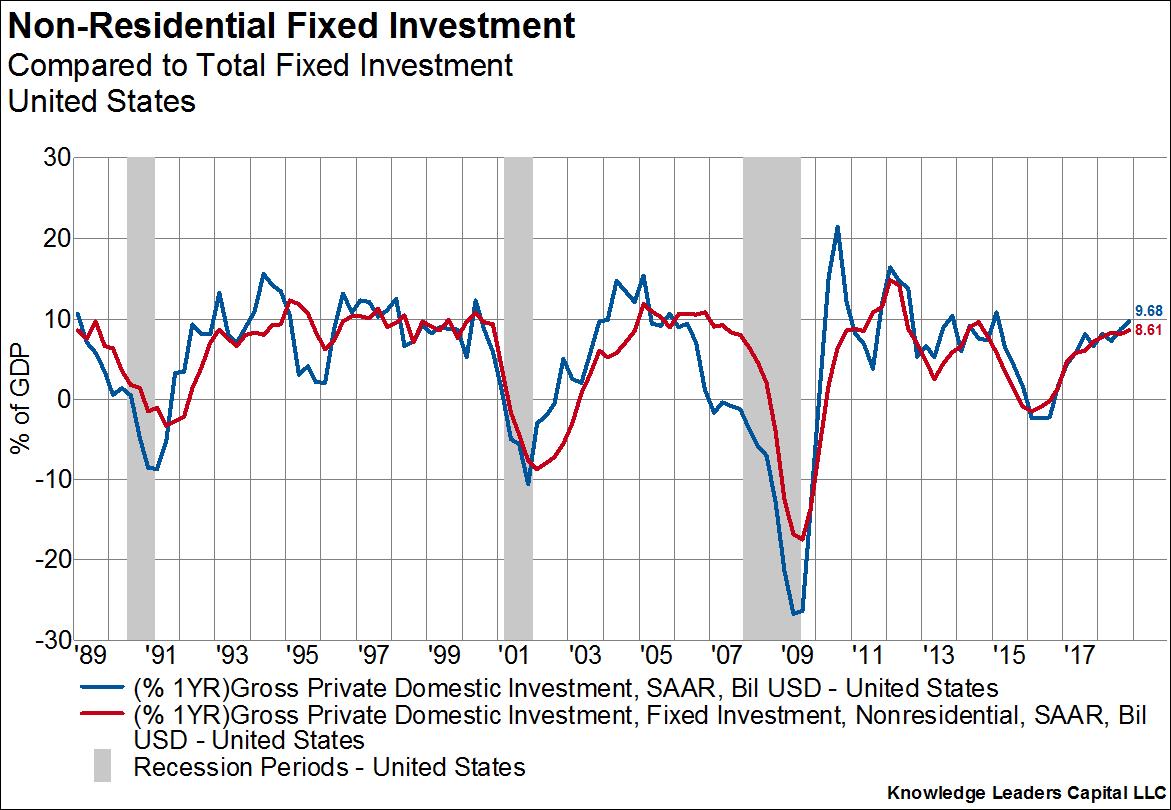

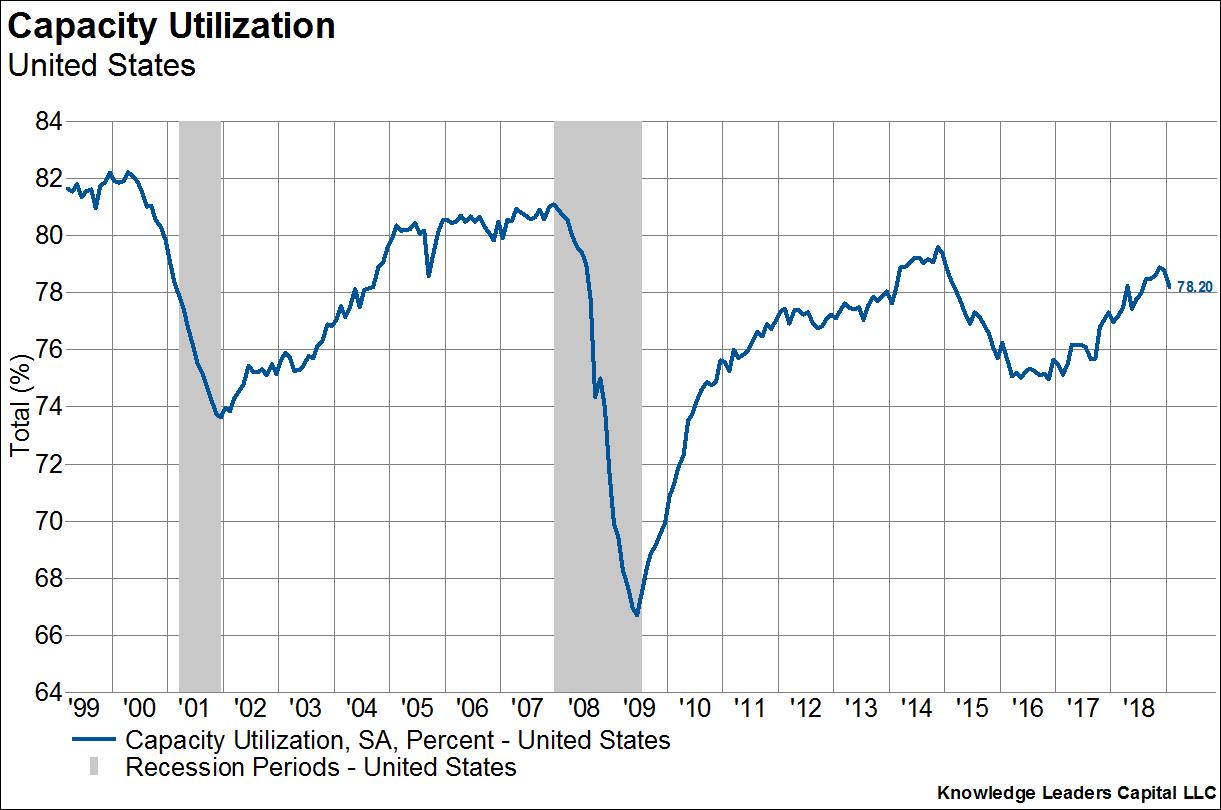

As an aside, think about this before I move on to the financial market implications. Capital spending has increased at a decent clip since the tax overhaul went into effect, but that trend started in 2016 before the tax cuts went into effect and the YoY growth in capex sits at a very average level for a late stage expansion. The reason of course is that capacity utilization remains low so there isn’t much need to expand aggressively to meet end demand. That is to say, much of the windfall from tax reform has gone strait to free cash flow (i.e. savings) which then get distributed to shareholders in the form of buybacks and dividends. The point is that if the capex incentives in the tax bill had actually spurred huge capital expansion then the trade deficit would be much much wider. But I digress.

We are more interested in the meaning of all this for financial markets. In our view it is the longer-term implications of running higher budget deficits lead in a near linear way (all else equal, which of course it is not) to a structurally lower dollar and foreign equity outperformance, with the possibility of a sprinkle of higher interest rates. Let’s take these one at a time.

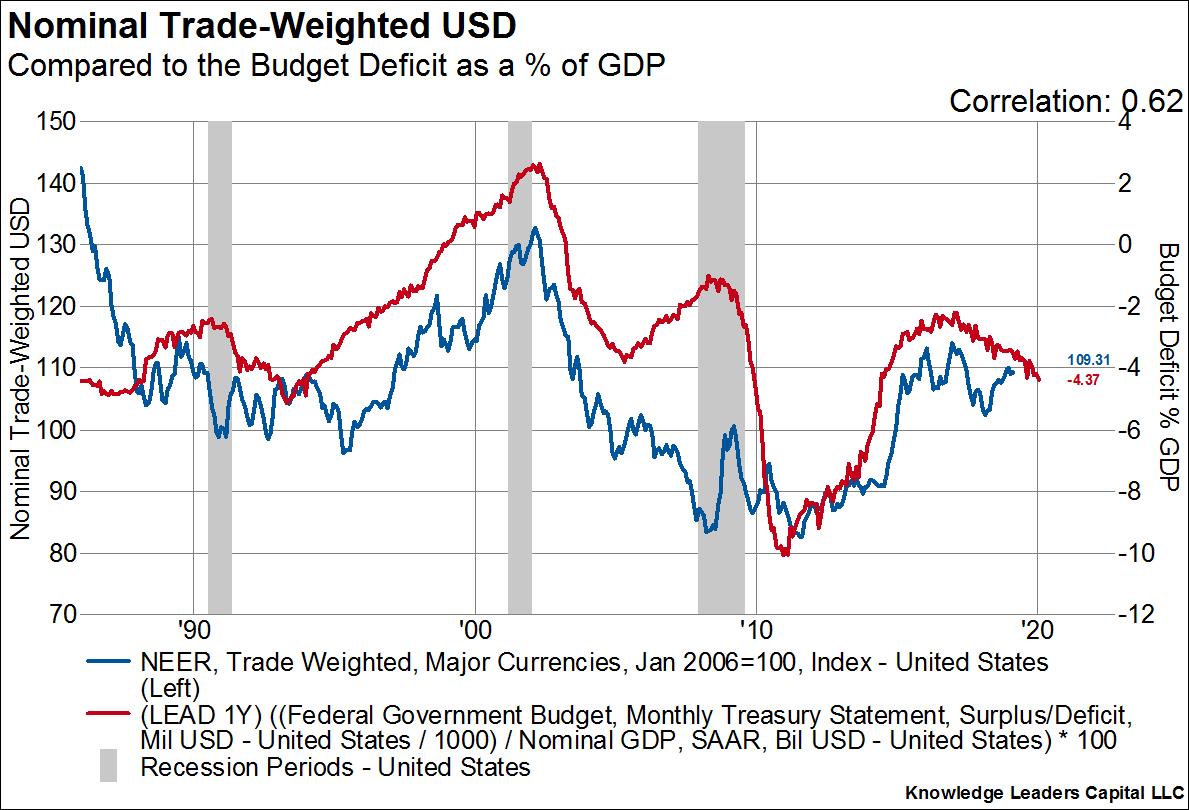

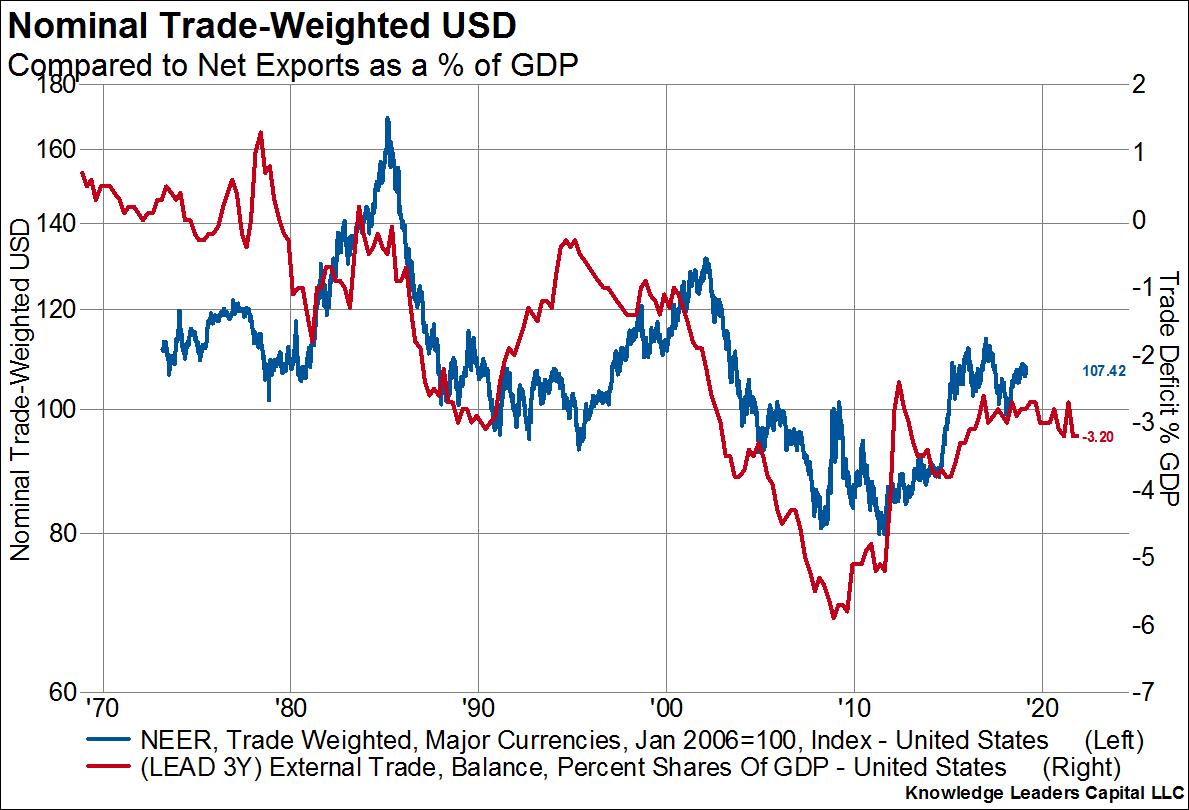

The dollar can rise and fall based on relative levels of inflation, growth, liquidity, or capital flows. It’s value is certainly more complicated than extrapolating changes in the budget and trade balance. Nonetheless, when trade and budget deficits are wide and widening, foreign investors require a dollar discount in order to finance the deficits. This is especially true if relative interest rate levels fail for whatever reason to compensate foreign investors for their risk. And so the dollar falls, thereby increasing the future ROIC on US dollar assets. We can see pretty clearly in the next two charts that both the budget deficit and trade deficit lead the value of the dollar by between 1-3 years. Both the budget and trade deficits are pointing to a lower dollar in the years ahead.

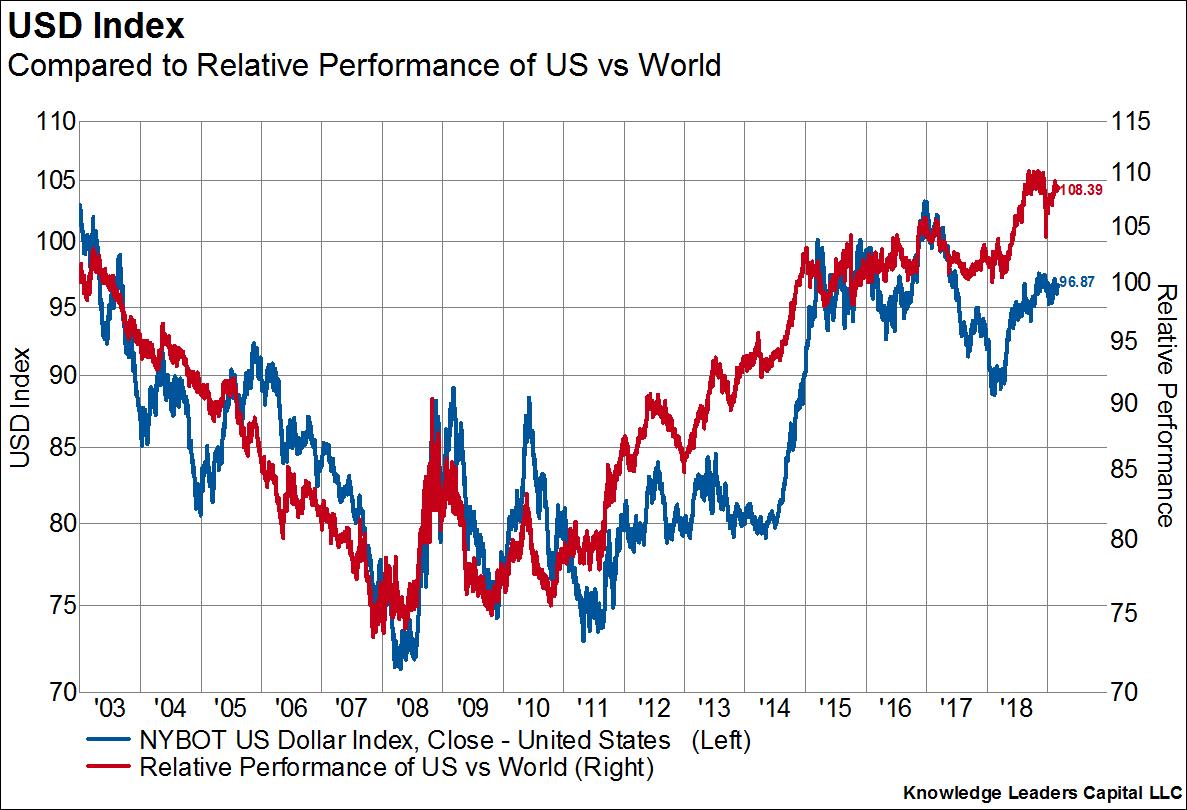

Moving on to stocks, the relative performance of foreign equities in US dollar terms is closely tied to the direction of the dollar, since a large portion of those returns are from the currency component. As we can see in the next chart, so goes the dollar, so goes the relative performance of US stocks vs foreign stocks.

The relationship between interest rates and the dollar is a bit murkier. Nonetheless, a structurally lower dollar should conceivably result in higher rates since foreign investors would want added compensation for expected currency depreciation. However, the size of the outstanding stock of debt and ever present possibility of the central bank buying more bonds would act as natural caps on the level of rates over the intermediate term.