Review of the Mathematical Distortions of Market Cap Weighted Indexes

February 17, 2015Earlier today we had a client ask us to verify a statistic they came across showing that the few largest companies in the world were responsible for the vast majority of the total return of the stock market over the last year. We took that prompt as a great opportunity to review the massive distortions created by market cap weighted indexes (which is most indexes).

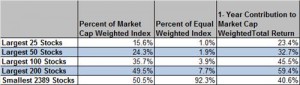

In the table below we break out the companies in the MSCI All Country World Index (ACWI) into buckets. We then compare the aggregate bucket market cap weighting in the index (2nd column) to the bucket’s percent of the index on an equal weighted basis (3rd column) and then finally we show the market cap weighted contribution to the total return of the ACWI over the last year (last column).

What we show is that the largest 25 companies in the ACWI comprise 15.6% of the market capitalization of the index, but on an equal weighted basis this group accounts for only 1% of all the investable stocks in this universe. Further, over the last year this small group of companies has accounted for 23% of the entire total return of this global benchmark.

Where things really get interesting is looking at the smallest 2389 stocks (out of 2589) that compose the ACWI. This group accounts for 92% of the developed and emerging market stock universe, but only accounts for 50% of the market capitalization of the index and only about 41% of the cap weighted total return of the index over the last year.

Needless to say, the capitalization weighting of the major global benchmarks can create some serious mathematical distortions that need to be considered by investors. From an investment execution perspective, investors need to be aware of the underlying position sizes and exposures created by market cap weighted ETFs and mutual funds.