A Checkup on the Yen & Leaderhisp Trends Among Japanese Stocks

March 25, 2015After two years of devaluation, the Japanese Yen is quite undervalued by our work. In the first chart below, we show the JP Morgan broad and narrow Japanese Yen relative to long-term trendlines. By these measures, the yen is around 25% below the 25 year average.

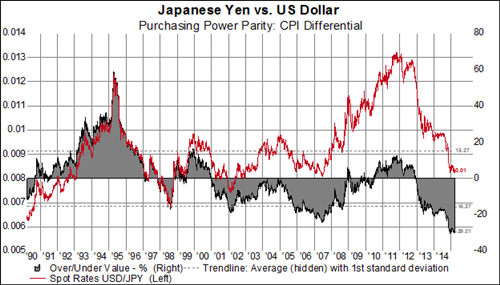

In this next chart, we show our purchasing power parity measure of the Yen. Here again, we calculate that the Yen is roughly 25-30% undervalued relative to the USD.

Historically, the Yen/USD has had a pretty good correlation with 2 year interest differentials. The spread in 2 year bonds tends to lead currency movements by roughly 18 months. Given the still small interest differential, this would suggest the possibility of Yen strength.

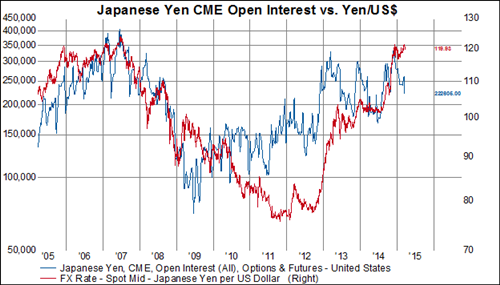

Since the beginning of the year, the open interest in JPY/USD derivatives has fallen by roughly a one-third.

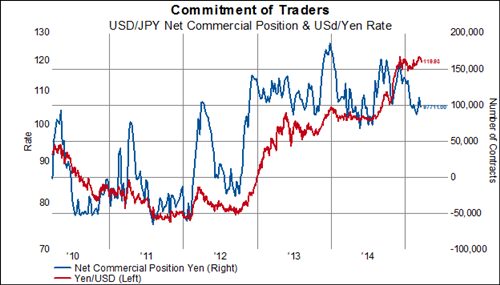

The positioning story is similar if we look at CFTC Commitment of Traders data. Net long positions on the USD/JPY have fallen by around 30% since the beginning of the year.

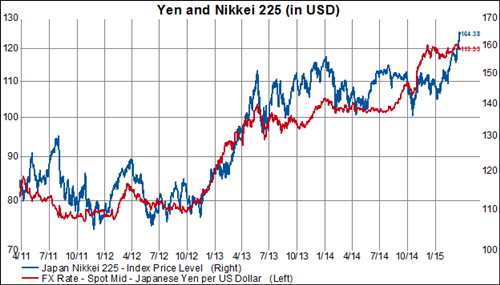

For the last few years, Japanese stocks have been joined at the hip to the Yen. That is until this year, where now Japanese stocks (in USD) are moving up in the absence of currency depreciation. This is a new dynamic.

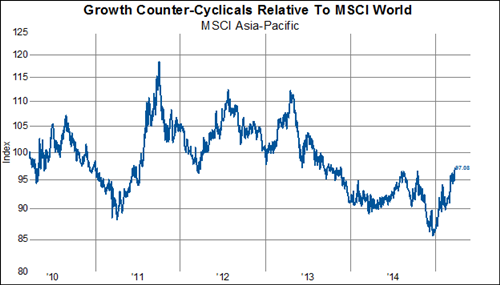

In this new dynamic, growth counter-cyclical stocks are the leadership group. In the chart below, we show Asia-Pacific growth counter-cyclicals relative to the MSCI World Index.

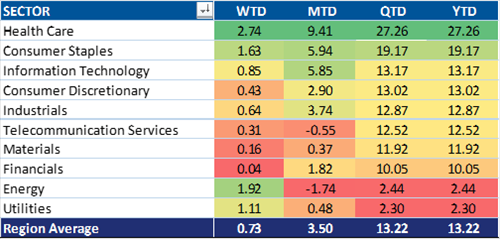

Of all the country-sectors in the MSCI World Index, the top two are Japanese health care and consumer staples.

MSCI Japan Sector Performance

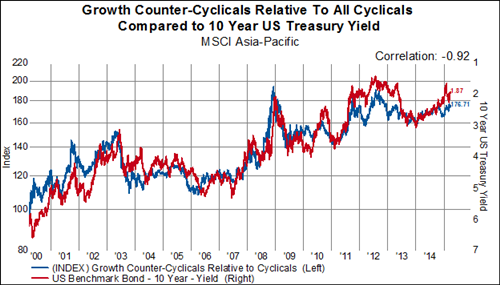

Perhaps helping to explain the appearance of shifting drivers of Japanese stocks, we show below the relationship between Asia-Pacific counter-cyclicals relative to cyclicals compared to US 10 year bonds. With a 15 year correlation of 92%, it is clear that US long rates are more important for Japanese stocks than the Yen. With a new move down in US long rates, it is easier to understand the move in Japanese counter-cyclicals this year. If US rates continue to drift down, even in the absence of further Yen weakness, it seems likely that Japanese health care and consumer staples will continue to outperform.