Runs, Slumps & Tactical Allocation

March 26, 2015Similar to a basketball player with a “hot hand”, stocks go on statistical runs. And similar to a player with a “cold streak”, stocks have slumps. Over time, with a proper perspective, it is easy to measure the extent to which these runs and slumps play out in the market and invest accordingly.

There are two components to the movements of all stocks: 1) the number of days up/down and 2) the average magnitude of the those daily moves. Over time, as the random walk hypothesis would project, stocks mean revert and are up 50% of the days and down 50% of the days. But, within this longer term mean reversion, stocks spend most of the time either above or below this 50% threshold, and this is the essence of measuring runs and slumps. Identifying stocks, sectors or countries that have deviated significantly from a random walk, and are expected to mean revert, can be helpful in making tactical allocation decisions.

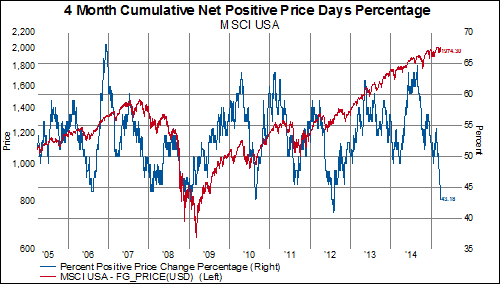

We take the trailing 88 trading days (4 months), measure everyday whether stocks were up or down for the day and accumulate this data into an 88 day running total. So, if a stock was up 50 out of the last 88 trading days and down 38 of those days, then it was up a net +12 days, or 57% of the days.

In the charts below, we show an example to demonstrate the methodology and how to use it to make tactical allocation decisions. In the first chart, we show the slump that MSCI US equities have been in lately. The current reading of -12 net days has only been met or exceeded twice in the last decade-in August 2010 and August 2012. Each time, this marked an intermediate low for US stocks.

Looked at on a percentage basis, MSCI US is only up 43% of the last 88 trading days. There is not one example over the last decade where the net percent of up days has fallen by over 20% in a six month period of time.

Given this huge statistical slump US equities have been in lately, perhaps it is time to tactically add to US positions. Mean reversion can be a powerful force to capitalize on in portfolio decisions.