A Reflationary Inflection in Oil Inventories

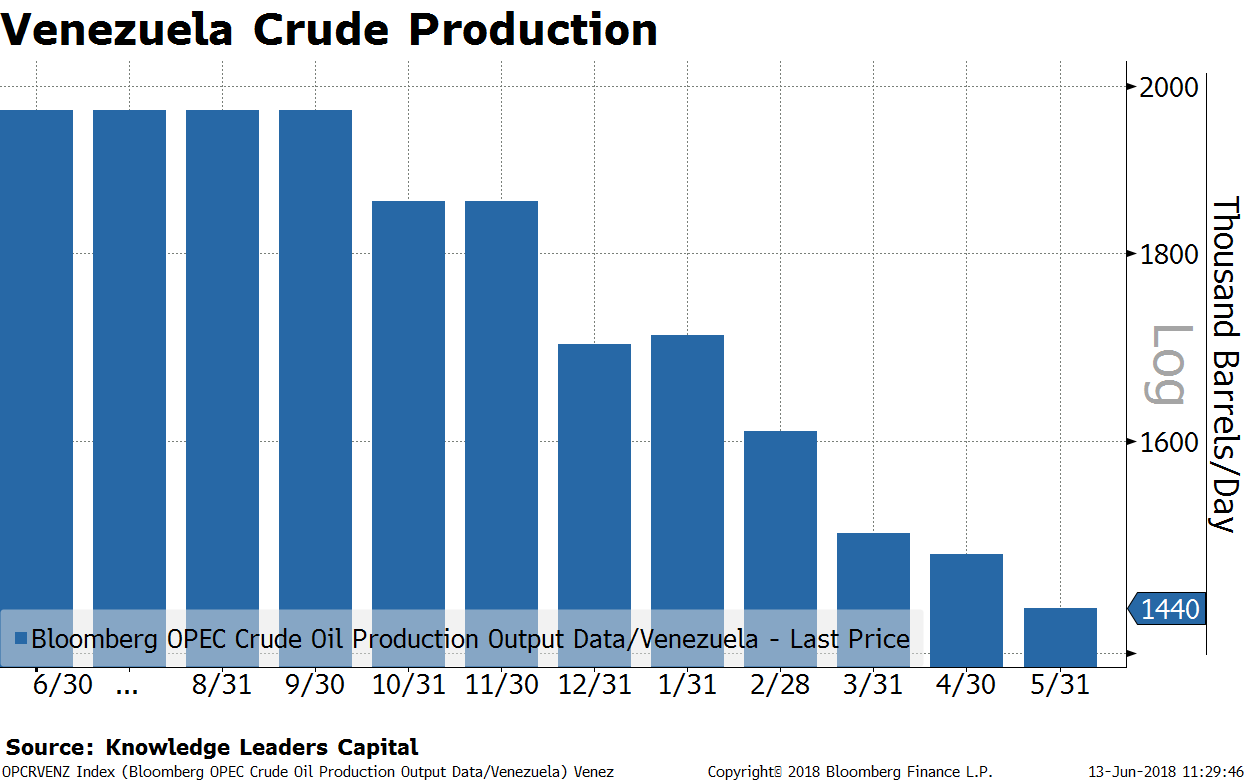

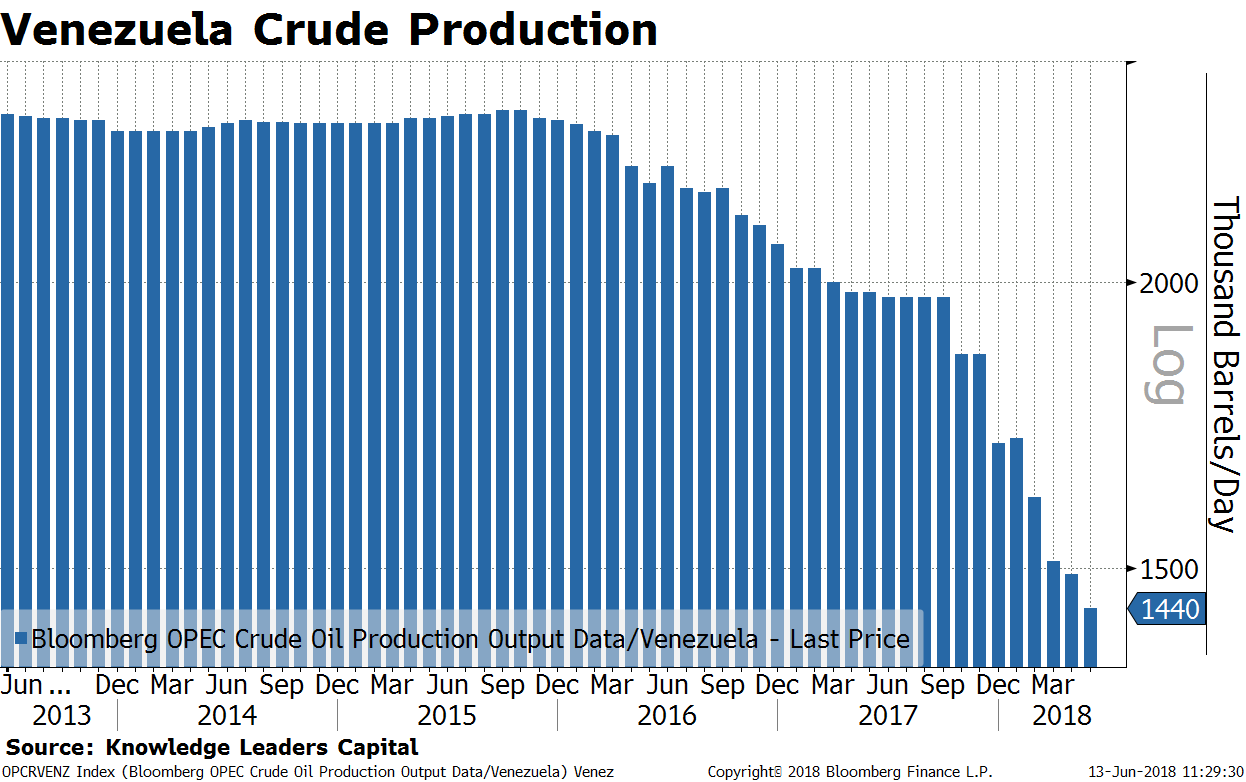

June 13, 2018Venezuela has experienced a collapse in oil production this year as the country sinks into chaos. Daily production is down from 1.7M barrels/day at the end of last year to just 1.44M barrels/day at the end of May. Year-over-year production declines are even larger, down about 500k barrels/day.

Production peaked in October 2015 at 2.38M barrels/day and is now roughly half that level.

U.S. Permian production (shale) has largely filled the void, with production up about 1.5M barrels/day since the peak in Venezuelan production. While Permian production is up about 1M barrels/day in the last year, it looks like transportation bottlenecks are starting to take their toll. The rate of increase in Permian production has slowed dramatically in the last few months, rising less than 100k barrels/day since March.

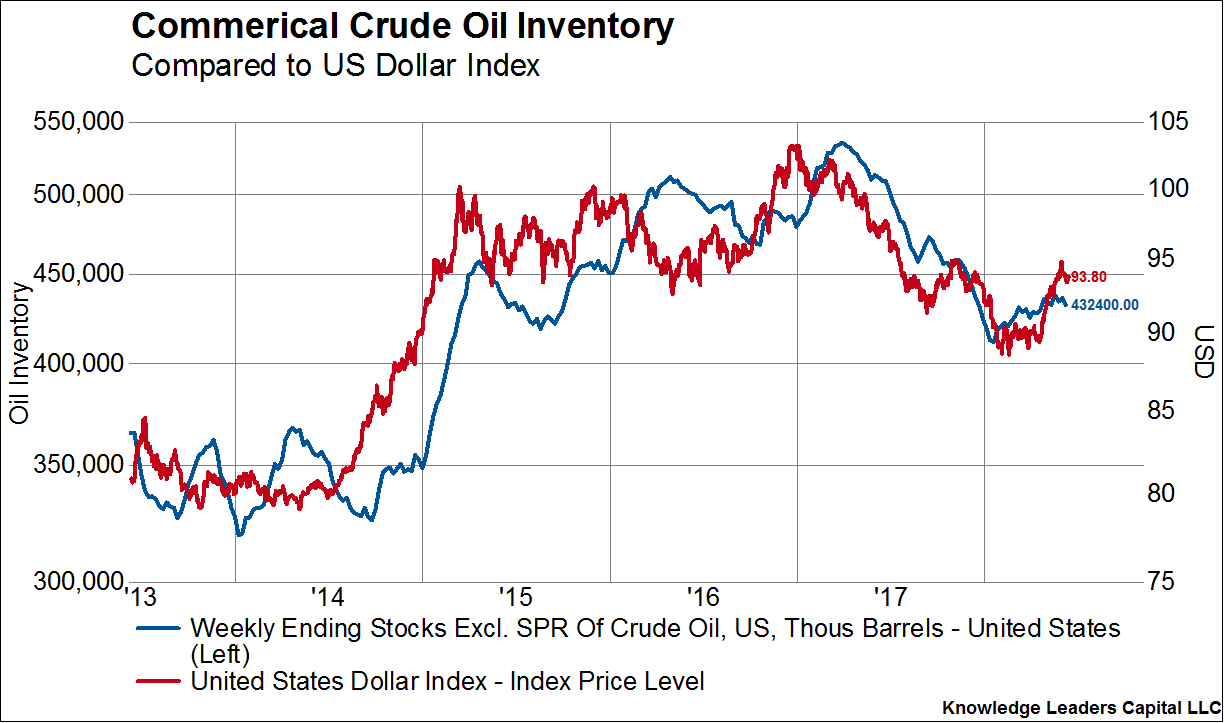

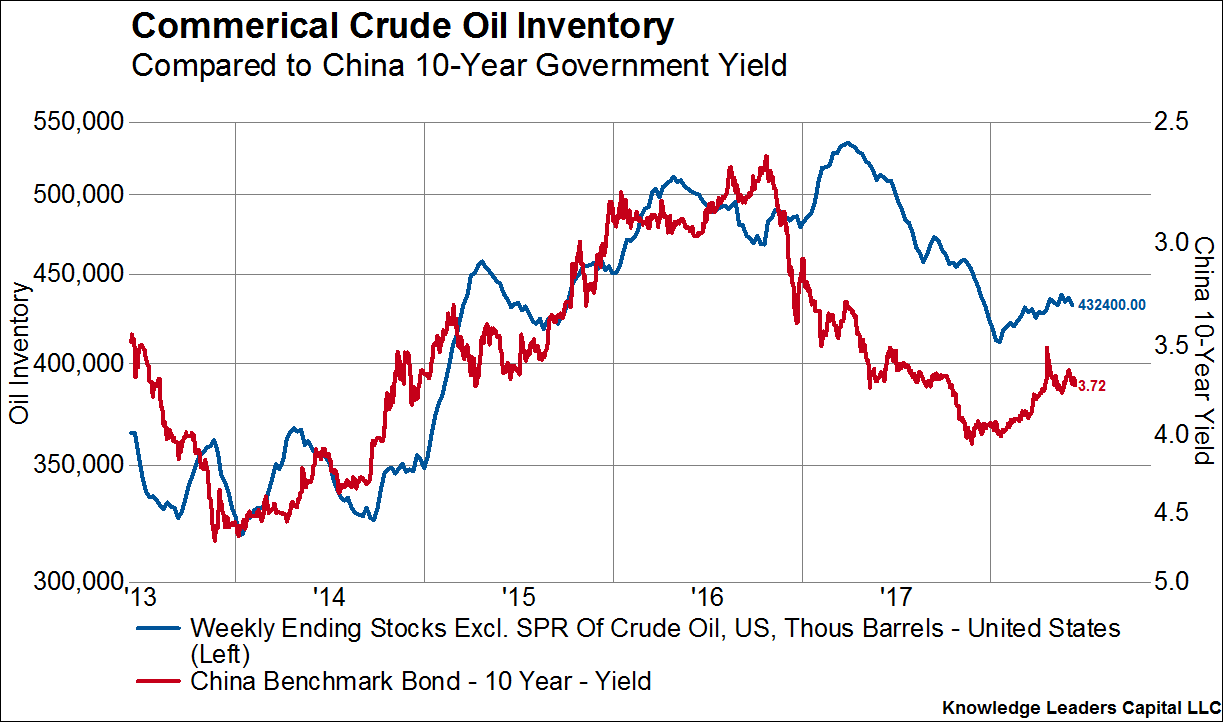

Today the Energy Information Agency (EIA) announced a drop in crude inventories in the last week. Crude inventories have been building most of the year, but in the last three weeks, we have experienced the largest inventory draw all year, perhaps reversing the trend of inventory builds. Crude supplies peaked May 18, 2018 at 438.132M barrels and now sit at 432.4M barrels.

If this is a durable change in the trend of inventories, I believe it has important consequences for the perception of the reflationary backdrop of the US and global economies. There are two important relationships I am watching here.

First, the shallow build in crude inventories this year has allowed the US Dollar to post a 5% counter-trend move. The performance of the USD has been tightly linked to oil prices for the last five years. When inventories built, the USD rose, and when inventories sank (like in 2017) the USD fell. The USD peaked on May 29 and has been sliding since.

Second is the relationship between crude inventories and the Chinese economy. All year, up until April 18, Chinese bond yields have been falling, suggesting some deflationary concern emanating from the Chinese economy.

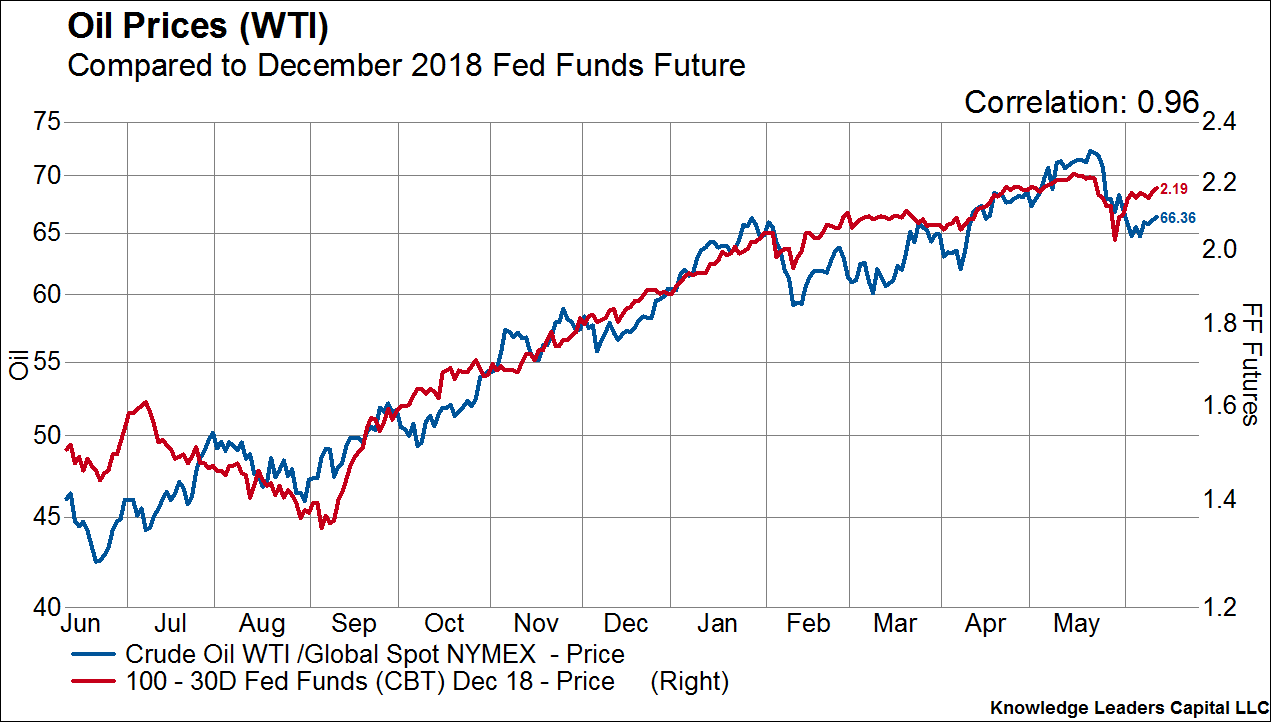

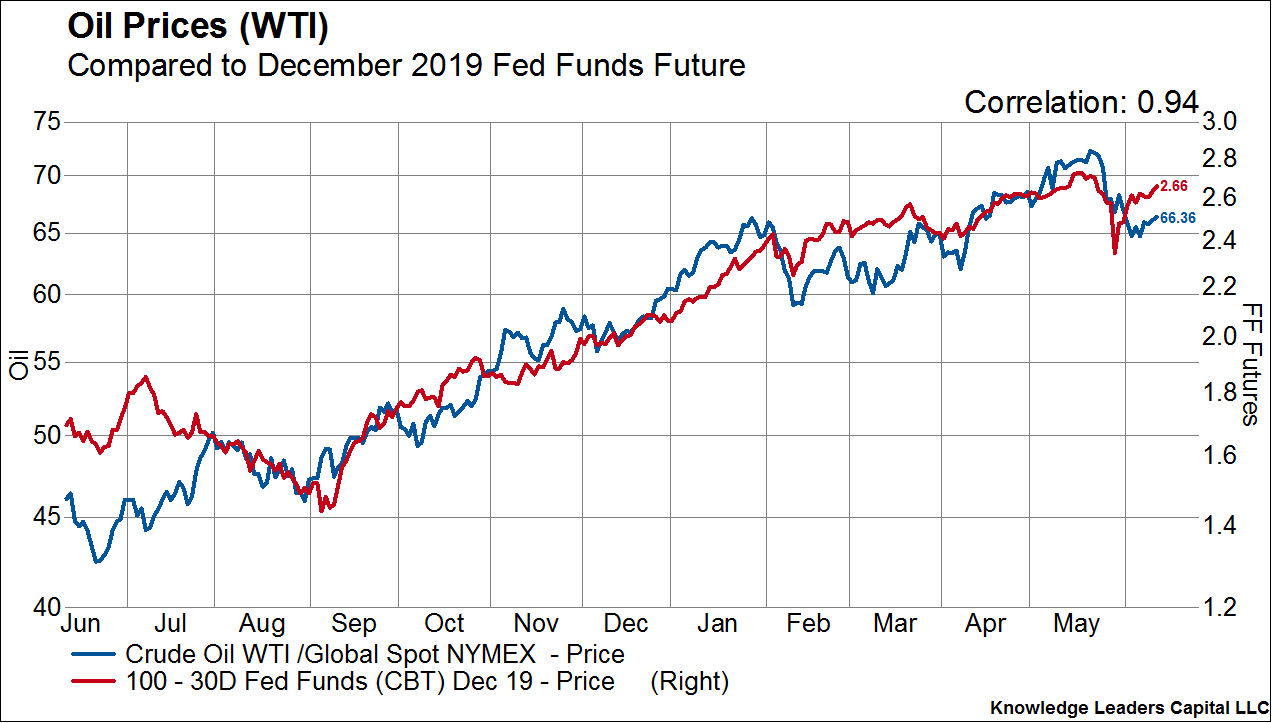

Oil prices have proved resilient this year, making steady gains even as inventories built slightly. Energy traders have likely correctly seen through the surge in Permian production, incorporating other factors like the decline in Venezuelan production. This is important because crude oil prices are one of the most correlated series to fed funds futures. In the chart below, I show the relationship over the last year. Crude and December 2018 fed funds futures have a 96% correlation. There is a 94% correlation between crude and December 2019 fed funds futures.

A continued rise in crude oil prices will surely keep the Federal Reserve on guard and may be the tipping point in favor of four rates hikes this year. If the supply/demand dynamics have changed in the crude oil markets, and trends of 2017 are about to reassert themselves, this should be seen as a reflationary inflection point. The result should be higher oil prices, higher inflation, higher rates and a lower US Dollar.