Are Commodities Signaling a Shift Away From US Equity Leadership?

August 08, 2018Most commodities have suffered lately with the backdrop of tariffs and China’s devaluation. But some have fared worse than others, and there is information content to the relative move in commodities. While copper catches many of the headlines (i.e. Dr. Copper, the metal with a Ph.D in economics) the most significant decline has occurred in lumber.

In general, copper goes into infrastructure kinds of fixed investments, things like the electric grid or telephone backbone. As the old joke goes, “where is the biggest copper mine?… under Manhattan.” Lumber, on the other hand, is used primarily in residential construction. Since most of the copper-intensive investments are going on in Asia and other developing markets, it is fair to say copper is a good proxy for economic activity outside the US. And since according to Edward Leamer’s working paper Housing IS the Business Cycle, it is fair to say lumber is a proxy for the health of the US economy. Not perfect, but a good shorthand.

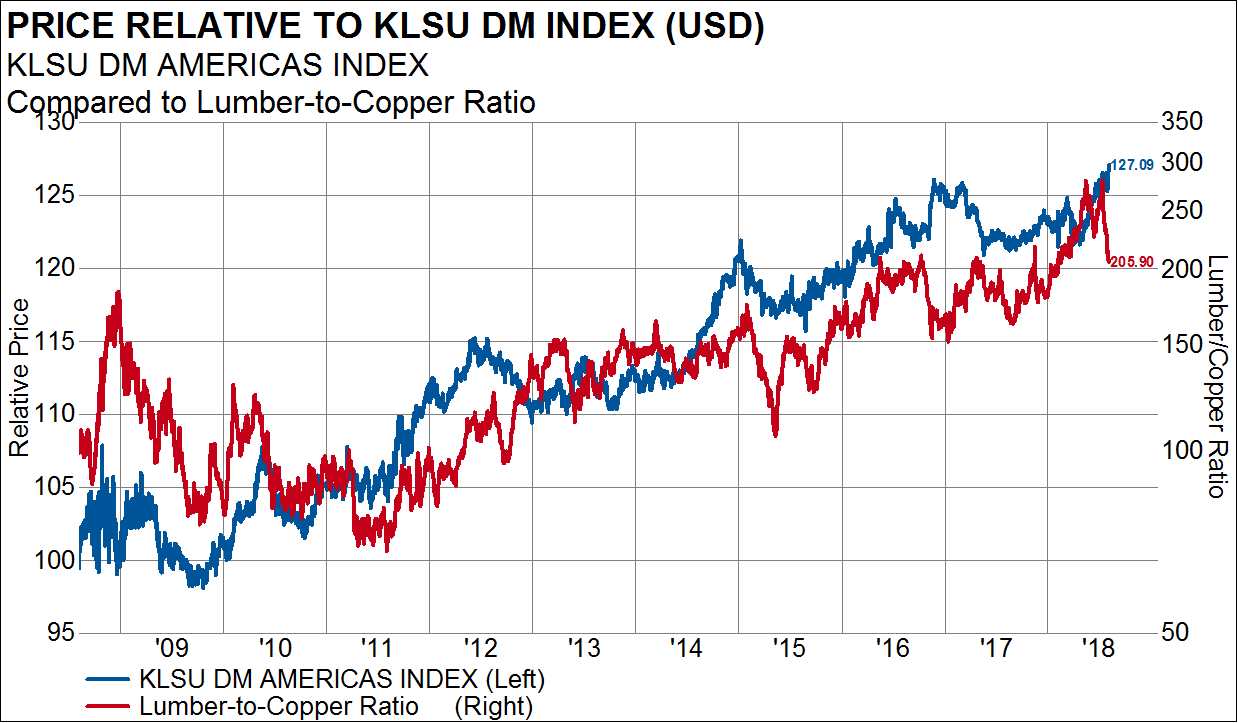

I construct a simple ratio of lumber to copper prices as a proxy for the health of the US vs. the rest of the world. In the next chart, I overlay the ratio on the performance of our KLSU Americas Index (top 85% of companies in North America) relative to the performance of our KLSU DM Index (top 85% of market cap of 22 developed countries). Each index is measured in USD and market-cap weighted. For the most part, oscillations in the lumber/copper ratio coincide with the relative performance of US stocks relative to the Developed World. From this perspective, the recent drop in the copper/lumber ratio should raise some red flags when thinking about continued US equity leadership.

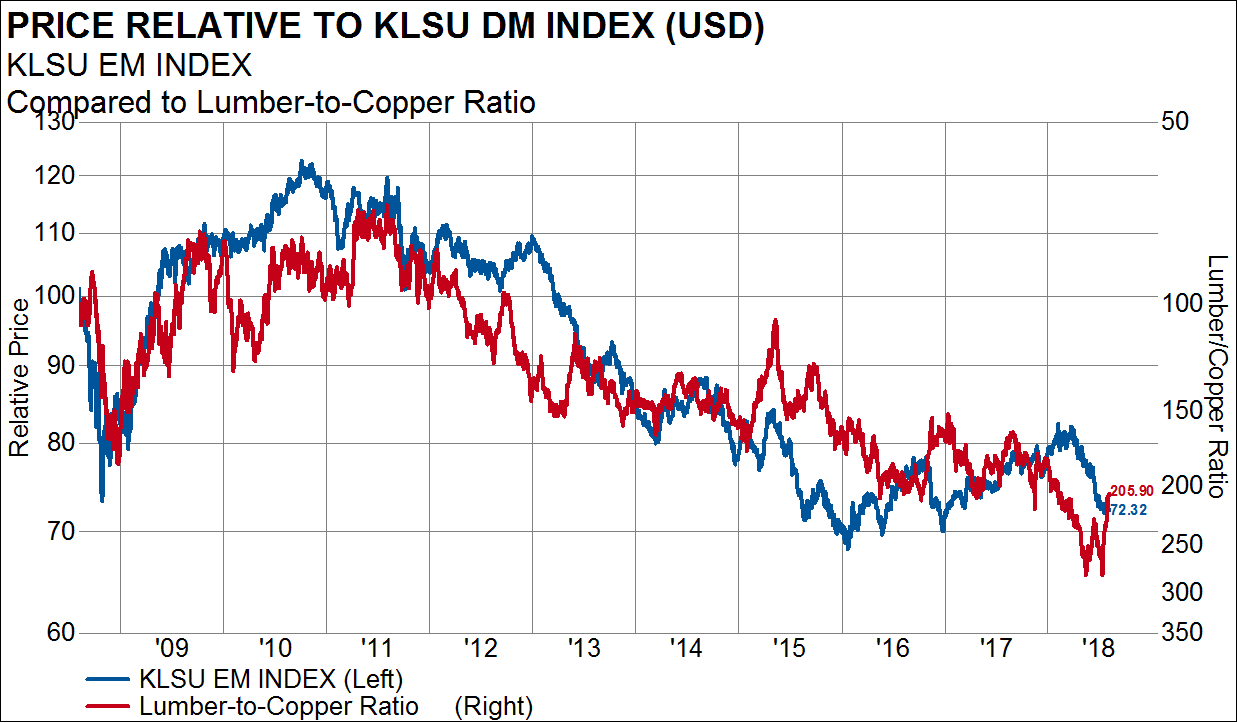

On the other hand, it does historically bode well for the relative performance of emerging markets. In the next chart, I simply invert the lumber/copper ratio and overlay on the relative performance of our KLSU EM Index (top 85% of 24 emerging market countries, in USD and market cap weighted also).

While most market watchers are convinced that the economic climate remains much better in the US than in the emerging markets, the commodity markets seem to be suggesting the possibility that the opposite may be true. Perhaps the decline in lumber reflects the ongoing slowdown in the US housing market. Housing starts (1,210k vs. 1,175k), building permits (1,320k vs. 1,292k), new home sales (636k vs. 631k) and existing home sales (5.6M vs. 5.4M) are all down since the start of the year.

As Leamer’s paper begins, “Of the components of GDP, residential investment offers by far the best early warning sign of an oncoming recession. Since World War II we have had eight recessions preceded by substantial problems in housing and consumer durables.”