There is a Huge Disconnect Between Energy Credit and Equity

November 13, 2018Oil prices have swung drastically over the last couple months. The market was unprepared for the US to grant waivers amounting to nearly one million barrels/day to fill the void expected to be left by the drop in Iranian exports. Instead of Iranian exports plunging to almost zero by November, they have been allowed a more shallow glide path. This has thrown the oil market off-balance by about one million barrels/day.

Especially strange is the fact that the US asked Saudi Arabia to pump another approximately one million barrels/day earlier in the year, and the Kingdom has delivered, taking OPEC’s production up by one million barrels/day since June. Yesterday, Saudi Arabia floated the idea of trimming OPEC’s production by one million barrels/day by December.

Adding to the oddities in the energy market is the nose-dive in US exports of petroleum products to China. Similar to disruptions seen in the soybean market, this seems to have a geopolitical undertone.

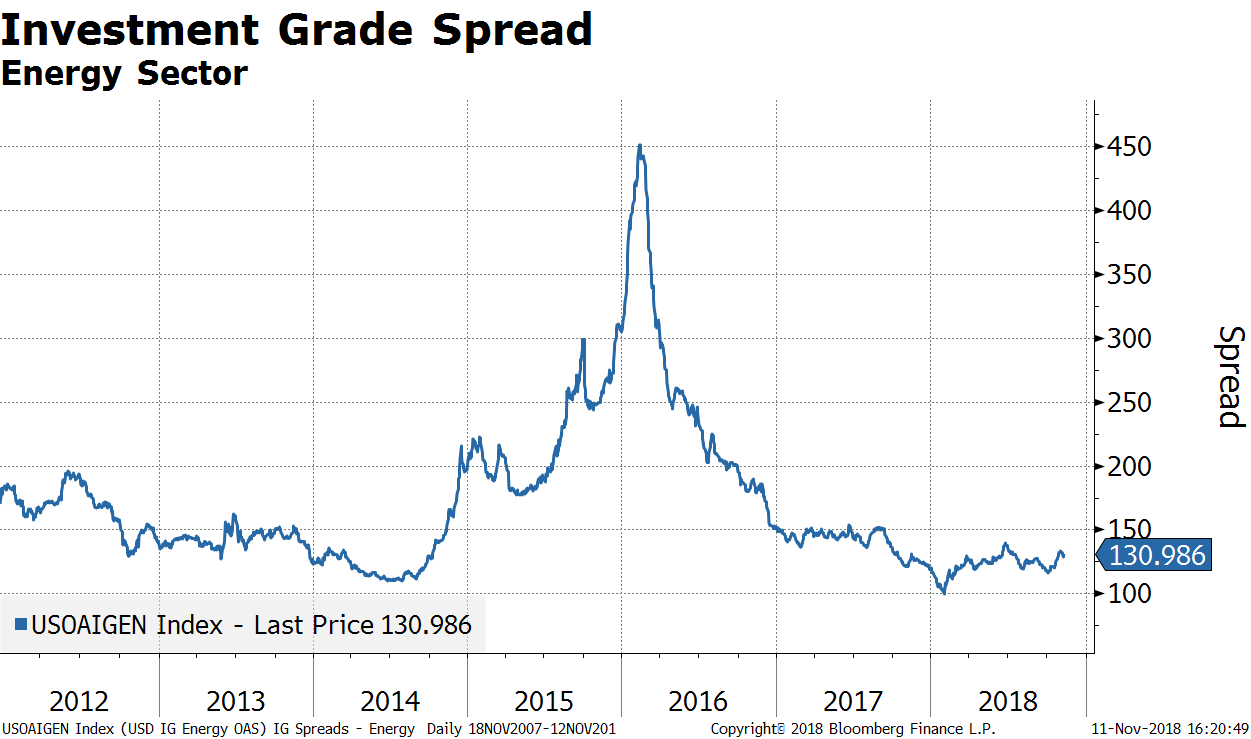

Turning to the credit markets, I can’t help but observe how tame energy-related credits have been recently given all the swings in commodity prices. Compared to 2015-16, when investment-grade energy spreads widened about 350bps to 450bps, recent moves are tame by comparison. The rise in spreads in October failed to match what we saw earlier in the year.

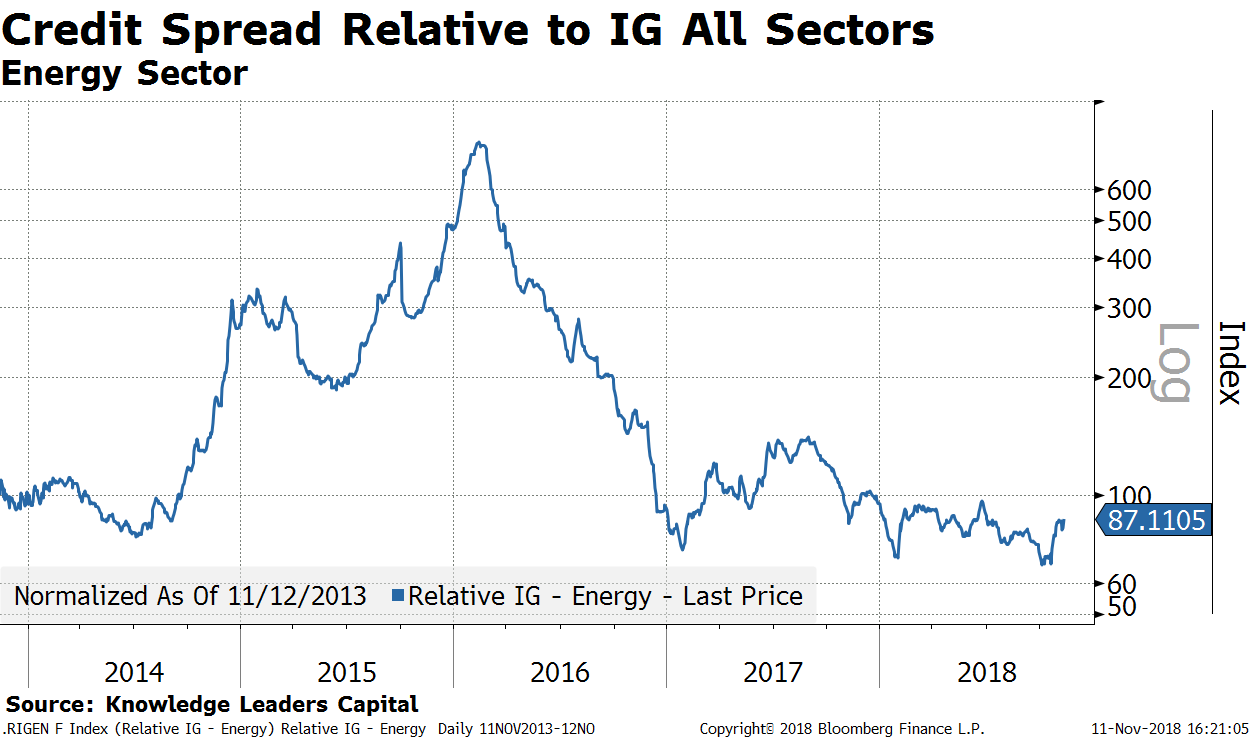

Energy credit relative to the broader investment-grade credit universe is behaving quite well. Relative credit spreads have actually narrowed this year, suggesting the energy sector is outperforming the broader corporate bond market.

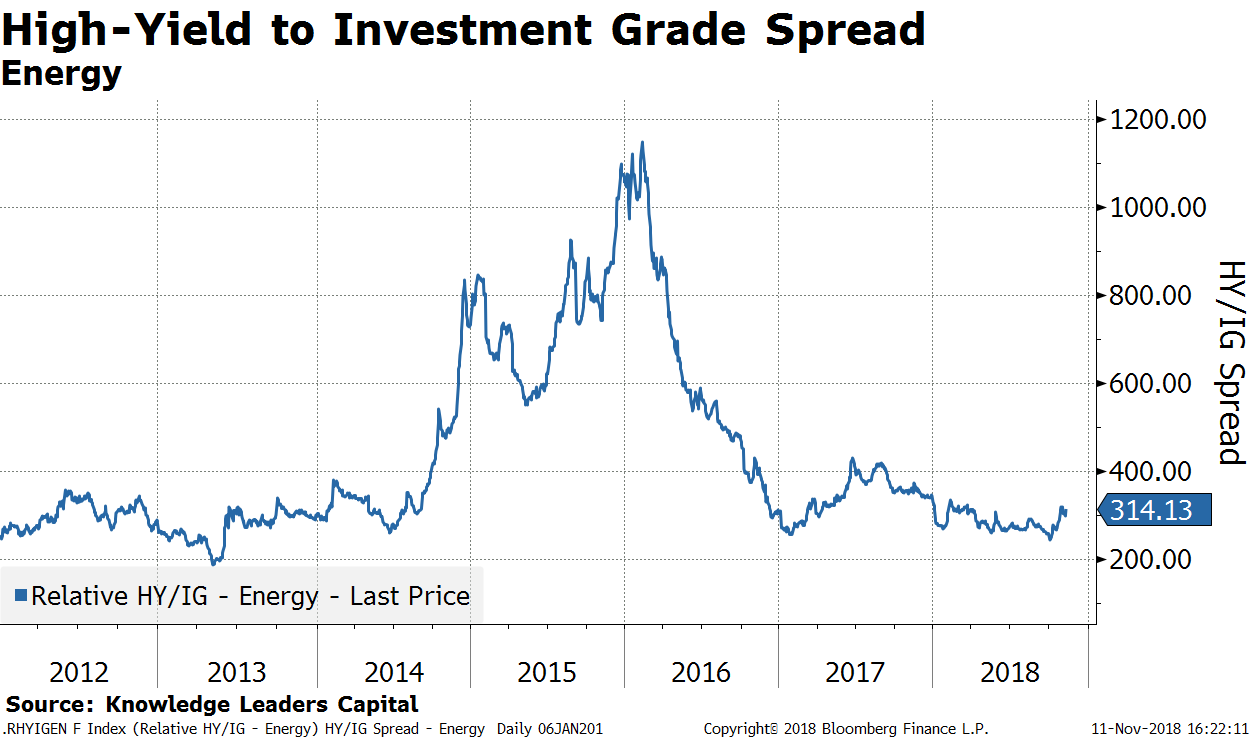

High-yield spreads have risen slightly recently, but they are down since the beginning of the year. High-yield spreads are back where they were when oil was $100/barrel in 2013.

The energy sector high-yield spread, compared to investment-grade spread, is also well-behaved and also down for the year. Energy high-yield credit is outperforming the broader investment-grade credit universe.

While not perfect, there tends be a relationship between relative credit spreads and relative equity outperformance. When spreads in a sector have narrowed relative to the broader corporate credit universe, this has tended to be coincident to the equities from this sector outperforming the S&P 500. Said differently, historically, when credit outperforms, stocks outperform.

The energy sector is so interesting to look at from this perspective. While energy credits are outperforming this year and have reverted to pre-2015 levels, the equities have not kept pace.

We see this when looking at the relative performance of high-yield spreads compared to equity relative performance also.

Investors in energy equities clearly fear a repeat of the 2015-16 bust, but that is unlikely for a variety of reasons. Importantly, the plunge in capital spending has already occurred and productivity (measured by production per working rig) is rising. Companies are again generating free cash flow, while holding down capital spending. Perhaps these are the data points credit investors see that equity investors don’t. Either way, there is a remarkably big disconnect between the behavior of energy bonds and stocks that could bode well for energy equities.