The Credit Markets Have Stalled

February 15, 2019Credit markets often move before the equity markets, and this can offer helpful information about the near-term path of equity prices. In general, I like to see credit confirming what the equity markets seem to be saying. When credit stalls, like it is now, I take notice.

Investment grade spreads recovered about 30bps between January 3 and February 5, 2019. They have since widened out by about 2bps while the equity market is mostly flat.

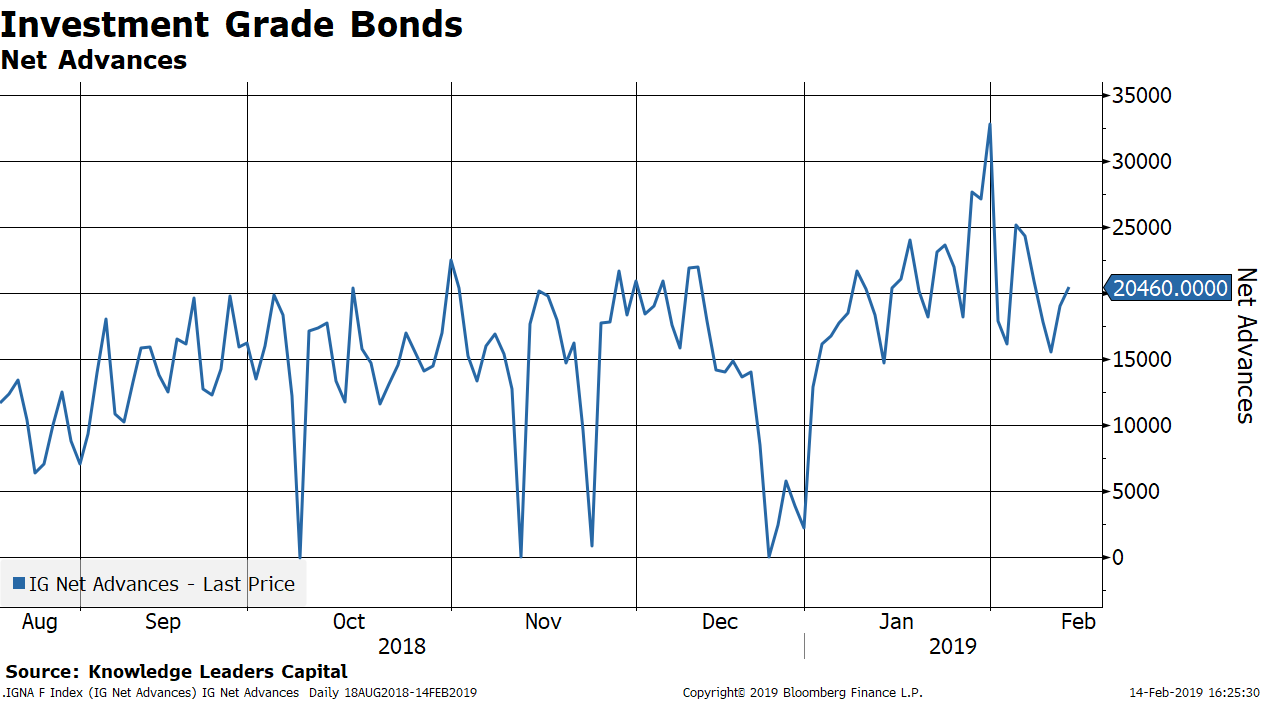

January was a strong month for corporate bonds of all stripes. After troughing at zero, net advances in the investment grade space surged to about 32,000 by the end of January. Net advances have since slipped back to about 20,000, a still healthy level.

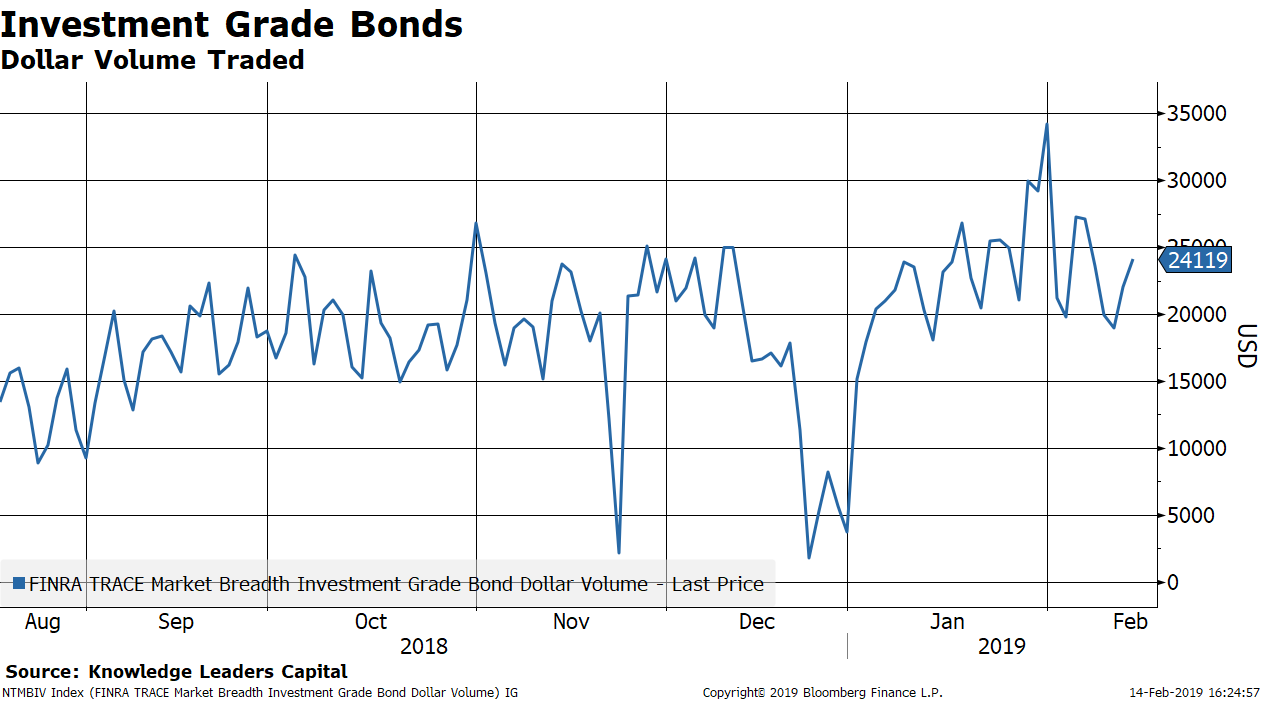

Bond traders were quite active in January after December’s chill. In the second half of December, trading volumes plunged as bonds fell, but they surged back to almost $35 billion per day at the end of January.

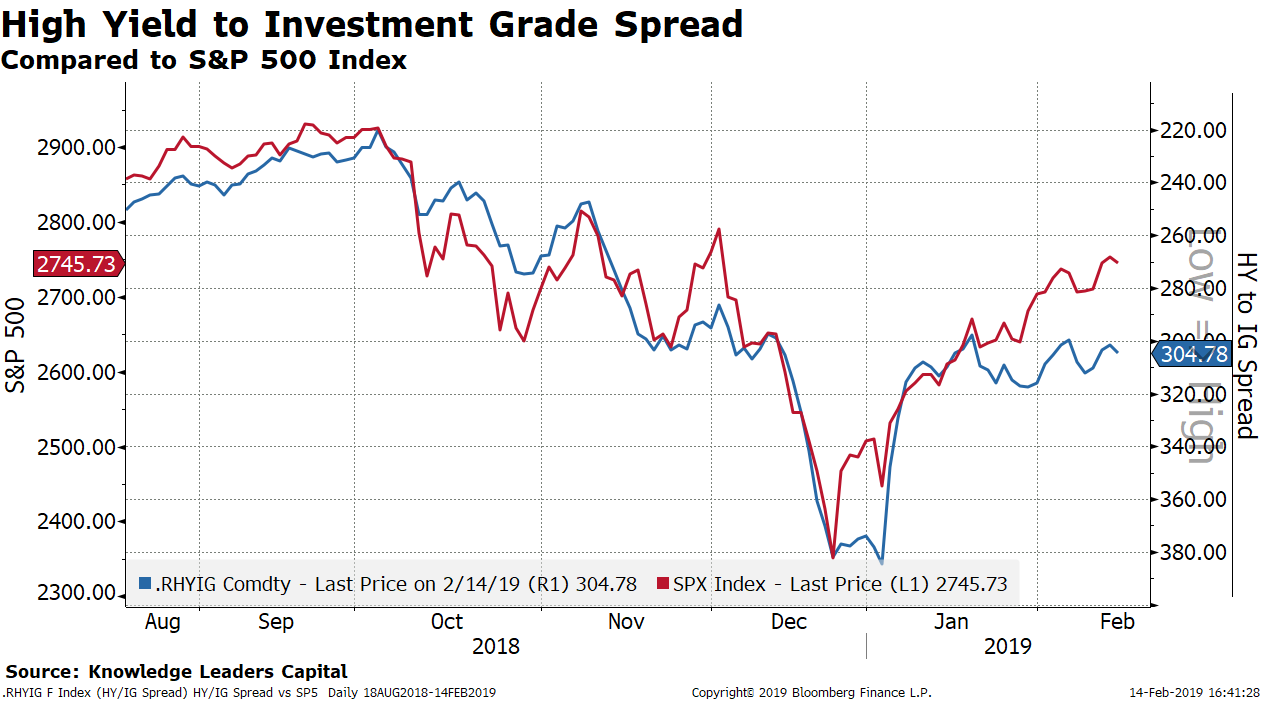

Because high-yield bonds trade more like stocks, I like to compare the relative spread between IG and HY to the S&P 500. High yield spreads stopped narrowing relative to investment grade on January 18, 2018.

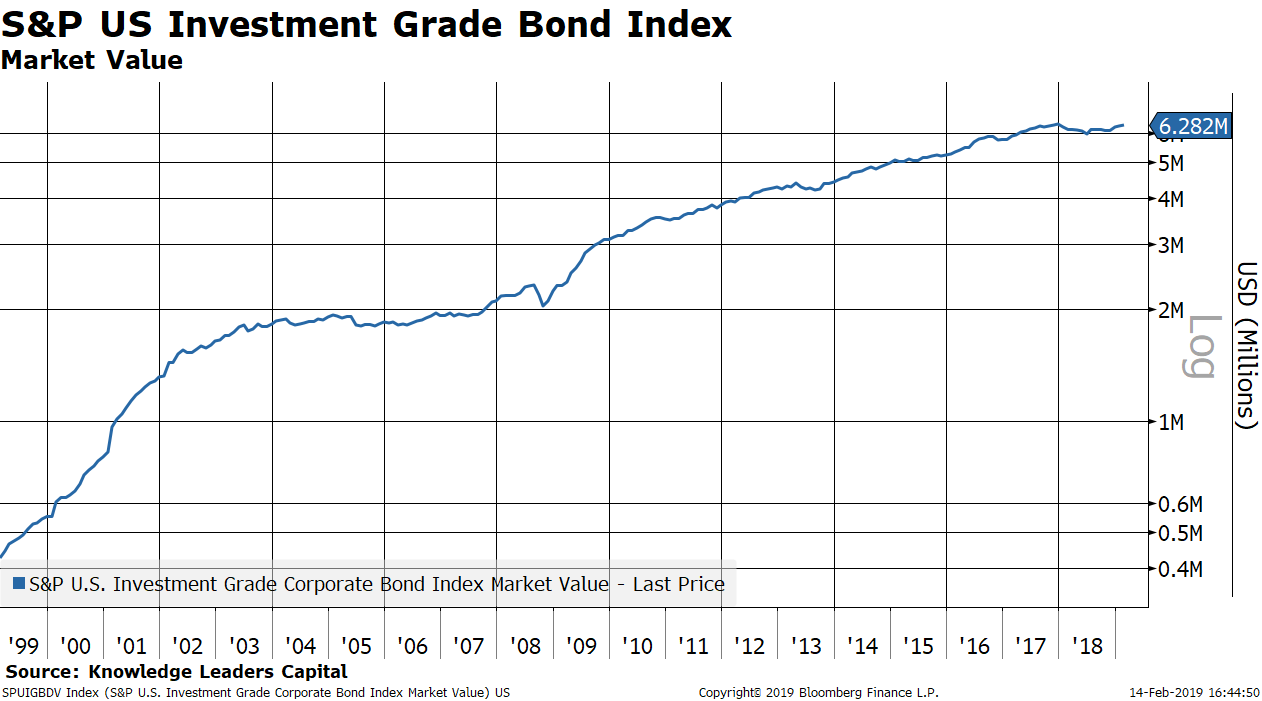

The divergent signs coming from credit are still early days but worth watching given that the US investment grade credit universe is over $6 trillion, roughly 3x the market value at the last recession and almost 10x the size of the 2001 recession.

The BBB weight, the lowest rung in investment grade, now constitutes 56% of the $6 trillion investment grade market, the highest in history.

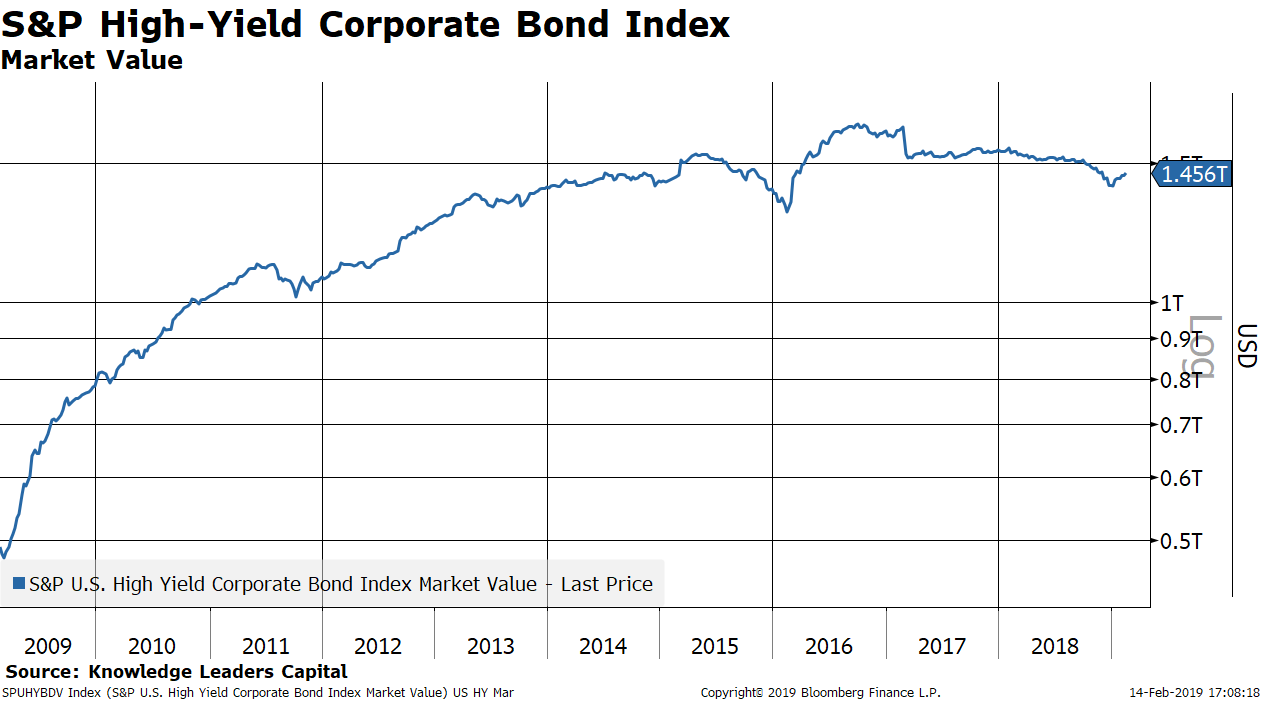

The high-yield market is only about $1.5 trillion, so a wave of credit downgrades could add significantly to this universe of credit, dragging down prices.

The longer the credit markets stall and diverge from equity markets, the more worried I become of a retesting sequence in the equity markets.