Regional Banks Face Headwinds

April 18, 2023This week as regional banks start reporting earnings we will get a better look at the lasting effects of the bank crisis kicked off by the failure of Silicon Valley Bank last month. Looking at recent earnings forecast revisions, regional banks appear particularly exposed to short- and longer-term headwinds.

So far this earnings season, larger banks have come out with stronger earnings than some expected. J.P. Morgan explicitly benefitted from receiving deposit inflows from stressed regional banks as well as having a more diversified business model. As of today, the broader bank sector as measured by the SPDR S&P Bank ETF (Ticker: KBE) has outperformed its regional bank counterpart, the SPDR S&P Regional Bank ETF (Ticker: KRE), by several percentage points this year.

Percent Price Decline YTD: KBE SPDR S&P Bank ETF vs. KRE SPDR S&P Regional Bank ETFs

This is no wonder considering the multiple challenges facing regional banks, including net interest income compression (due to the demand for higher yield deposit accounts), higher exposure to troubled commercial real estate, and a lack of diversification in their business model, not to mention increased competition from fintech, which now includes the likes of a Goldman Sachs-sponsored Apple Savings account yielding 4.15%.

Below, I’ll look at how challenges born by regional banks have already fed into sales and earnings estimates for this year and next in the form of estimate revisions for the current fiscal year. I start by taking the top 85% of companies from both countries by market cap and then filter for large and mid-cap diversified and regional bank stocks in United States. I omit Canada here because regional banks make up a larger part of the financial system in the US than in Canada, which is dominated by large, heavily regulated banks. The result is a mid-large cap universe of 144 financial companies, including 26 regional banks and 12 diversified banks.

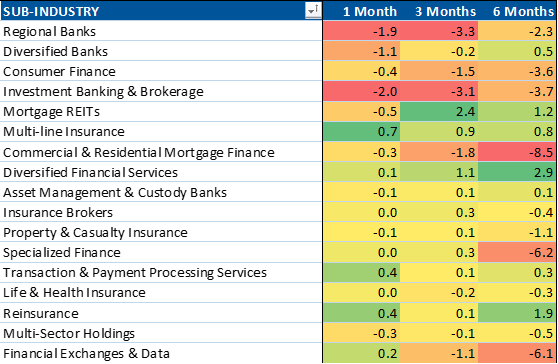

So far, over the past 3 months, regional banks in our universe have seen this year’s sales estimates (FY1) hurt more than any other financials sub-industry, according to our proprietary analysis tools.

Change in FY1 Sales Estimates (%) for the Current Fiscal Year:

Sales estimate revisions for next year also are down an additional 2.6% in the last month for regional banks, the most for all financial stocks in our universe. This is a recognition by regional bank analysts that regional banks now face several additional hurdles that could negatively affect revenues for years.

Change in FY2 Sales Estimates (%) for the current Fiscal Year

Earnings-per-share (FY1) estimate revisions haven’t been any better for regional banks this year, ranking second lowest in downward revision percentage in the last month, after sharp downgrades three and six months ago.

Change in FY1 EPS Estimates (%) for the Current Fiscal Year

The most recent revisions to FY2 estimates are the worst for regional banks, signaling no let up in their diminished status going forward.

Change in FY2 EPS Estimates (%) for Next Fiscal Year

We already have seen the market price in some of the headwinds to which regional banks are particularly exposed. Regional bank earnings results and outlooks this earnings season could give investors a better understanding of just how damaged their future prospects could be.

As of 3/31/23, none of the securities mentioned were held in the Knowledge Leaders Strategy.