A Contrary Opinion On The US Employment Report

February 06, 2015

By in News

One of the main features of the current recovery is the drop in the potential growth rate. In every other recovery since WW2, real GDP has risen back to potential as the recovery got going, thereby closing the output gap. This time around, the output gap has narrowed because potential GDP has been revised down. This is an important point to understand when looking at today’s jobs report.

Real GDP, Potential GDP and Long-term GDP Trend

GDP has basically two ingredients: 1) productivity and 2) labor force growth. Estimates of potential growth are a function of estimates of these two variables. In mid-January the CBO released its latest projections of real GDP for 2015-2025. They estimate potential real GDP over the next decade at 2.1%, with .5% coming from labor force growth and 1.6% coming from labor productivity.

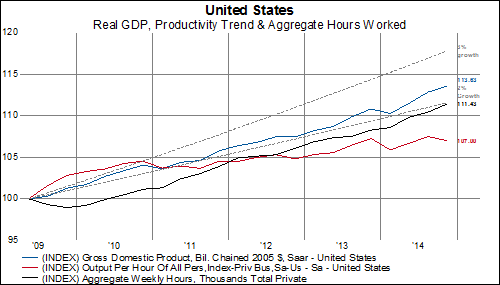

With this framework in mind, one of the interesting features of the recent GDP report and labor market reports, is the recent stagnation in productivity. For the private sector, productivity was basically flat last year while aggregate hours worked by private sector employees rose by almost 3.5%. Of that 3.5%, roughly 2.3% came from new jobs…and hence the excitement surrounding today’s job numbers. Looking back at private sector productivity, hours worked and total real GDP since 2009, we can see an interesting pattern emerge. The first phase of the recovery-from 2009 through 2010-productivity surged and represented more than 100% of total economic growth. But then productivity slowed in 2011-2013, and in 2014 it flat lined. Will it decline in 2015?

In 2014, the entirety of real GDP growth came from more hours worked rather than greater productivity. While it is good news that the labor force grew by 1.1% year over year in January, in December the one year growth rate was .7%. So, looking back at 2014 and using the annual performance of the US economy, we can see that potential growth was really running closer to .7% (productivity + labor force growth). There are least four conclusions to draw from this:

1) With real GDP running closer to a 3% rate in 2014, the economy is growing beyond potential right now. This raises the spectre of inflationary pressures building and helps explain the sharp sell-off in US Treasury bonds.

2) This also should get the Federal Reserve’s attention and helps explain the big drop in December 2015 fed funds futures. This should bring fed fund increases sooner.

3) If this stagnation in productivity continues, it may pose a challenge for corporate profits and capital investment.

4) If this productivity stagnation continues, long-term estimates of the speed limit of the US economy need to be adjusted down again.

It is great news that the US is creating more jobs, but it is much worse news for the economy that productivity is stagnating. As Paul Krugman once said, “Productivity isn’t everything, but it is nearly everything.”

Tags > employment