A Few Signs Are Pointing To A Lower US Savings Rate In 2015

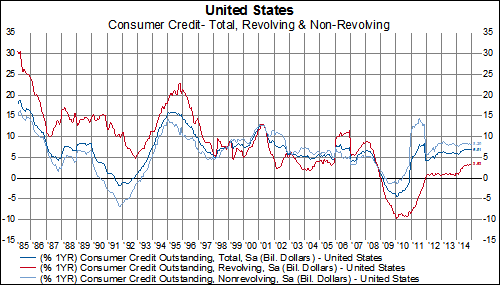

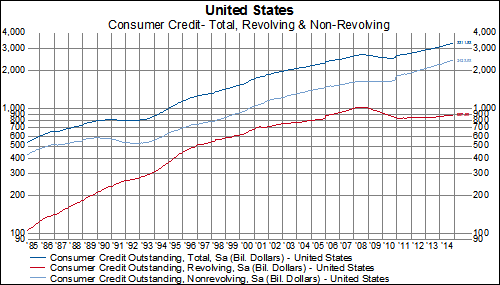

February 06, 2015Since the depths of the financial crisis, the rebound in consumer credit has been polarized. On the one hand you have non-revolving consumer credit (i.e. car loans, student loans, etc.), which briefly declined on a year-over-year basis in 2009 and early 2010 before violently rebounding in 2011. Over the past two years, non-revolving consumer credit has consistently grown at an approximately 8% year-over-year rate. On the other hand, you have revolving consumer credit (i.e. credit cards) which plunged in 2009 and continued to decline on a year-over-year basis until the end of 2011. In 2012 and 2013 revolving credit stopped declining but only grew at approximately a 1% rate. However, finally in 2014, revolving credit bounced back and steadily increased all year long. It finished the year growing at a 3.5% year-over-year rate, the highest such rate since 2008. It should be noted that this is still well below the 8% year-over-year growth rate that revolving credit has averaged over the past 30 years. Combined together, consumer credit grew by 6.9% in 2014.

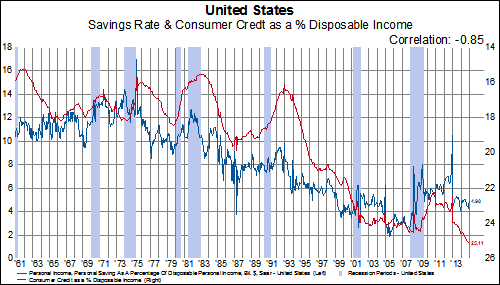

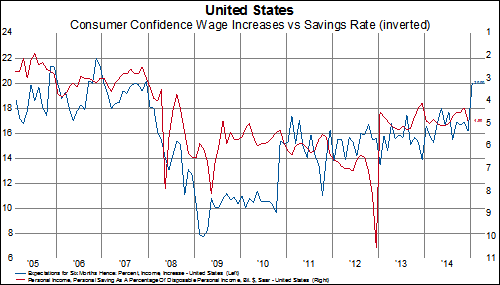

However, this increase in consumer credit may be a negative sign for the personal savings rate in the US. Consumer credit as a percentage of disposable income reached an all-time high in 2014. At the end of December, consumer credit equaled 25.1% of annualized disposable personal income. This has had a highly negative correlation to the savings rate (-0.85) since 1960 and we would not be surprised to see the savings rate decline further. In addition, the highest percentage of consumers are confident that they will receive a raise in the next six months since December 2007. Over the past decade, the more consumers that expect a raise the lower the savings rate tends to be.