What is Driving US Treasury Rates Lower in 2020?

January 29, 202010-Year US Treasury yields are down about 30bps so far this year, continuing the trend of lower rates that began in the fall of 2018 and confounding investor expectations for rising rates which would validate a turn up in economic activity.

The primary driver of the decline in rates is the term premium. With oil prices falling, the inflation risk component of the term premium, which is highly correlated with oil, has fallen by about 15bps. Our models using petroleum inventories suggest the inflation risk premium should be around -40bps.

The 15bps decline in the real rate risk premium reflects increasing odds that the Fed will be pushed to cut rates again this year. December 2021 fed funds futures are now pricing in one full cut in rates this fall.

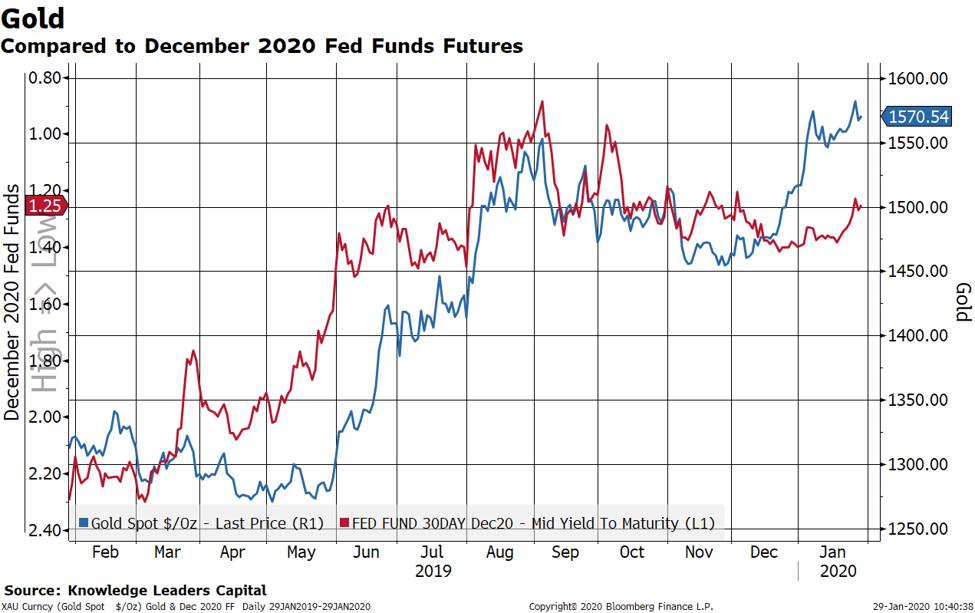

Our expectations of fed cuts in 2020 are strengthened by the breakout in gold we’ve seen recently. Gold and fed funds tend to move in tandem, so the breakout in gold validates the market’s expectation for at least one cut in the fed funds rate this year and suggests fed funds could end the year at 1%.

So, to summarize, the drivers of lower rates this year are:

-Tumbling oil (and other commodity) prices, taking the term premium down by about 15bps. Is this a reflection of a weaker global economic outlook?

-Growing expectations for additional interest rate cuts this year, taking the real rate risk premium down by an additional 15bps. Despite the fact that Phase 1 of the China trade deal is complete and USMCA is signed, perhaps US economic growth is languishing from damage already done by the trade conflict and/or will suffer negative repercussions from the Coronavirus outbreak.