Ready for Another USD Rally?

June 19, 2020As funding strains appeared in March, the USD surged. Then the Fed stepped in with massive foreign exchange swaps as a way to lend USD to foreign central banks, intended to ultimately be lent to borrowers in need of USD. As F/X swaps reached almost $500 billion, allocated heavily to Japan and Europe, the USD experienced a 7% correction, from 1,300 on the BBDXY to 1,200.

Now, as liquidity strains have been addressed, the F/X swaps are rolling off, leading to an outright decline in the Fed’s balance sheet last week. As the swaps roll off, the USD is rising again, up about 2% in the last couple weeks.

In our opinion, had the F/X swaps not occurred the USD was naturally on a glide path higher as petroleum inventories went through the roof. The BBDXY has a pretty good historic fit with the inventory of petroleum products—both crude and refined—not including the Strategic Petroleum Reserve (SPR).

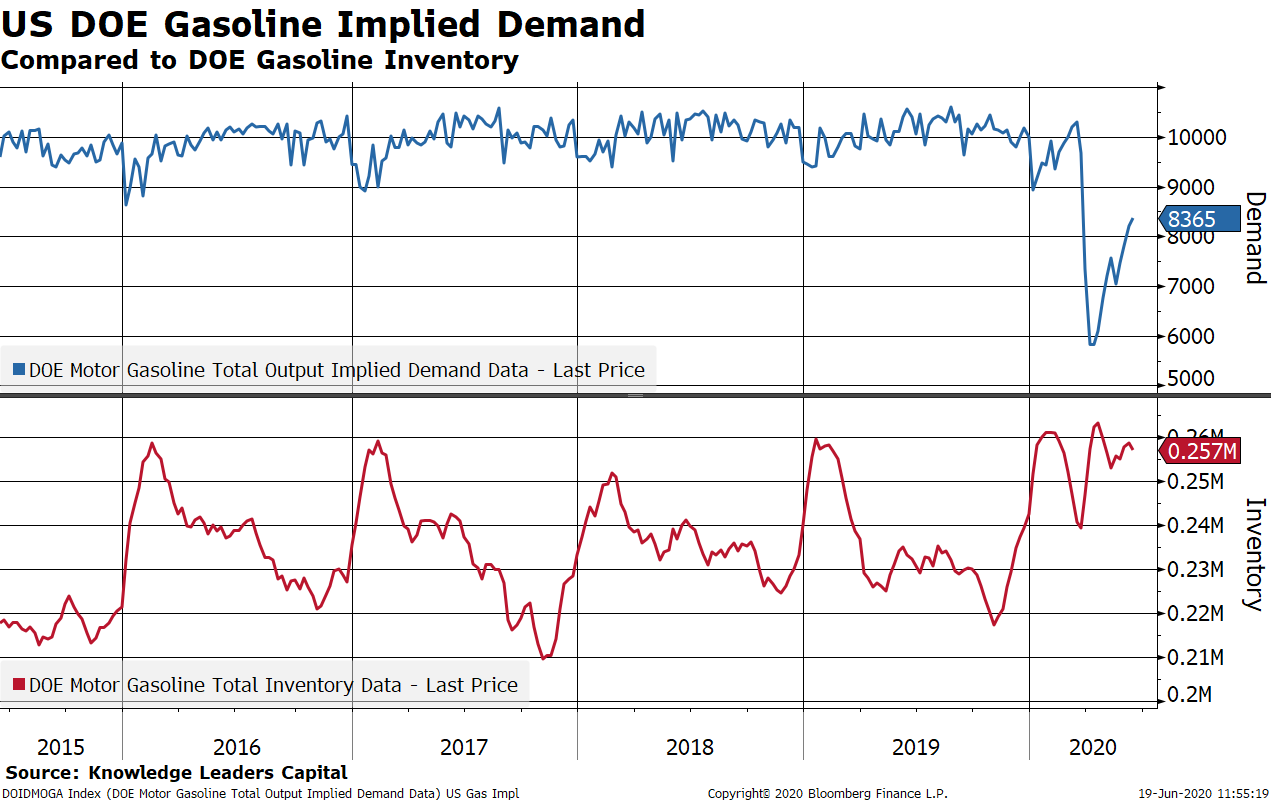

To give some perspective on the distortions the COVID-19 crisis has created in the energy markets, US gasoline inventories are totally out of whack from a seasonal standpoint. Inventories tend to peak in the winter and draw through the fall as driving picks up with warmer weather.

With daily gasoline demand still some 20% below year-ago levels, inventories in June are hanging around the highs for the year, while they should be down around 100-200 million barrels from winter peaks.

The level of petroleum inventories suggests the BBDXY at 1,300, or about 5% higher from here. If the F/X swaps are sunsetting, then perhaps fundamentals may re-assert themselves and we should be ready for a continuation of the USD rally.